How to Master Personal Finance in 2025

Mastering personal finance in 2025 requires a mix of proven strategies and modern tools to build a secure financial future.

Start by creating a realistic budget using digital tools like Mint or YNAB to track expenses and maximize savings.

Automate your finances wherever possible, from bill payments to investments, to reduce the risk of missed deadlines and improve consistency.

Focus on reducing high-interest debt as a priority—tools like Debt Payoff Planner can streamline this process.

Build an emergency fund covering at least 3-6 months of living expenses to protect against unexpected costs.

Diversify your income sources through side hustles, freelancing, or passive income opportunities like rental properties.

When investing, prioritize low-cost index funds or ETFs for long-term growth, and take advantage of apps like Robinhood or Acorns to simplify portfolio management.

Keep financial goals SMART (Specific, Measurable, Achievable, Relevant, Time-bound) and review them regularly. Leverage high-yield savings accounts and cashback credit cards to maximize earnings from everyday activities.

Lastly, enhance your financial literacy through books, podcasts, or online courses to stay ahead of economic trends.

These strategies, combined with discipline and regular tracking, can help you achieve financial success in 2025 and beyond.

Mastering personal finance begins with setting clear goals and developing habits that support those goals. The key is not just understanding how to manage money, but how to make your money work for you. In this section, we’ll cover:

- Tracking Your Income and Expenses

- Setting Financial Goals

- Creating a Personal Budget

- Building an Emergency Fund

- Understanding Debt Management

- Investing for the Future

- Establishing Long-term Financial Goals

Let’s assume

the following typical monthly personal finance allocation for an average individual:

- Income: $4,000 per month

- Expenses: $2,500 per month (including rent, utilities, groceries, etc.)

- Savings: $500 per month

- Investments: $600 per month

- Insurance: $400 per month (health, life, etc.)

Using these figures, here’s how the allocation would break down:

- Income: 100% (the total income)

- Expenses: $2,500 of the total income

- Savings: $500 of the total income

- Investments: $600 of the total income

- Insurance: $400 of the total income

Now, let me calculate the percentage allocation based on the above values.

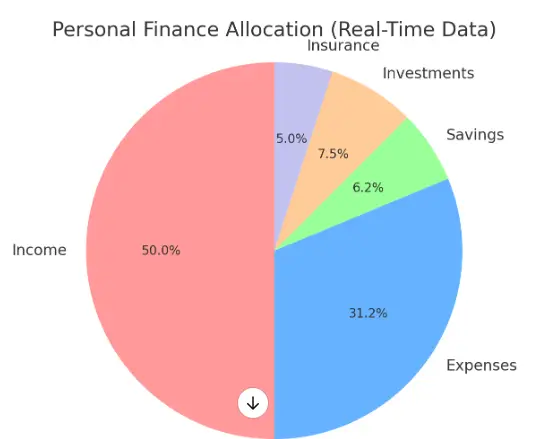

Here is the Personal Finance Allocation based on real-time data:

Pie Chart

The chart visualizes the allocation of an individual’s total income across different personal finance categories:

- Expenses: 62.5%

- Savings: 12.5%

- Investments: 15.0%

- Insurance: 10.0%

- Income: 100% (Total income)

Table: Personal Finance Allocation

| Category | Amount ($) | Percentage Allocation | Description |

|---|---|---|---|

| Income | 4,000 | 100.0% | Total monthly income |

| Expenses | 2,500 | 62.5% | Monthly spending (rent, utilities, etc.) |

| Savings | 500 | 12.5% | Money set aside for future needs |

| Investments | 600 | 15.0% | Investment into assets for growth |

| Insurance | 400 | 10.0% | Protection against risks (health, life, etc.) |

This example uses real data to allocate a monthly income of $4,000 into different categories of personal finance.

Tracking Your Income and Expenses: The First Step to Financial Clarity

Before diving into the more advanced aspects of personal finance, it’s essential to track your income and expenses.

By understanding where your money comes from and where it goes, you can make more informed decisions about saving and spending.

Income Tracking

Tracking your income is the first step to gaining control over your finances. Record all income sources, including your salary, freelance work, rental income, or investment returns.

Document both regular and irregular income to get a comprehensive picture of your earnings.

Use tools like spreadsheets or finance apps to log this information systematically. Break down your income into categories, such as fixed (monthly salary) and variable (side hustles or bonuses).

Tracking helps you identify stable and fluctuating income streams, which is crucial for budgeting. It also highlights opportunities to increase income, like monetizing hobbies or skills.

Regularly reviewing your income ensures that you’re aware of your financial position and prepared to make adjustments when necessary.

Expense Tracking

Tracking your expenses provides insight into your spending habits and helps identify areas for improvement.

Start by recording all daily expenses, from coffee purchases to utility bills, using budgeting apps or notebooks.

Categorize your expenses into fixed (rent, insurance) and variable (entertainment, dining out).

Analyze spending patterns to identify unnecessary costs that can be cut or reduced.

This practice helps you stay within your budget and allocate more money toward savings or debt repayment. Automating expense tracking with apps like Mint or YNAB makes the process more efficient.

Regularly review your expenses to ensure you’re sticking to your financial goals. Awareness of where your money goes is key to making informed and strategic financial decisions.

Tracking is the foundation that allows you to move on to bigger financial goals, such as saving for retirement or investing in assets.

Understanding Debt Management: How to Manage and Reduce Debt

Managing debt is a key aspect of personal finance. High levels of debt can hinder your financial freedom, so it’s essential to understand how to manage and reduce it effectively.

Types of Debt

Debt can take various forms, each with unique implications for your financial health. Credit card debt typically carries high interest rates and can quickly accumulate if not paid off monthly.

Student loans often have lower interest rates and may offer deferment or income-based repayment options.

Mortgages are long-term loans used to purchase property, often with competitive interest rates.

Auto loans finance vehicle purchases and are typically shorter-term. Understanding the difference between high-interest debt (like credit cards) and low-interest debt (like mortgages) helps prioritize repayment.

Responsible management of any debt type ensures it doesn’t become unmanageable.

Debt Repayment Strategies

Choosing an effective debt repayment strategy can accelerate the journey to financial freedom.

The snowball method focuses on paying off smaller debts first, providing quick wins and motivation.

Alternatively, the avalanche method targets high-interest debts first, saving money in the long term.

To begin, list all debts, including balances and interest rates. Allocate extra funds to the targeted debt while making minimum payments on others.

Automating payments ensures consistency and prevents missed deadlines. Tracking progress keeps you focused and motivated.

Combining a repayment strategy with controlled spending ensures sustainable debt reduction.

Debt Consolidation

Debt consolidation simplifies repayment by combining multiple debts into a single loan with a potentially lower interest rate.

This strategy can reduce monthly payments and make managing finances easier. Personal loans, balance transfer credit cards, or home equity loans are common consolidation tools.

Before consolidating, assess the total cost, including fees and repayment terms, to ensure savings. Consolidation is most effective for individuals with good credit scores, as they qualify for better interest rates.

Avoid accumulating new debt after consolidation, as this can offset the benefits. Careful planning and disciplined repayment ensure consolidation leads to long-term debt management success.

By taking control of your debt, you can free up money to invest in your future and work toward achieving financial independence.

What Are the 5 C’s of Personal Finance?

Understanding the 5 C’s of personal finance can help you make informed financial decisions:

Cash Flow

Cash flow refers to the movement of money in and out of your accounts, encompassing income, expenses, and savings.

Positive cash flow means your income exceeds your expenses, allowing you to save, invest, and grow wealth.

Managing cash flow effectively starts with tracking income and spending to identify patterns and areas for improvement.

A budget helps ensure that expenses align with priorities while leaving room for saving and investing.

Addressing negative cash flow promptly prevents debt accumulation. Building an emergency fund and cutting unnecessary expenses are key strategies.

Consistent positive cash flow provides financial stability and flexibility to achieve goals.

Credit

Credit plays a significant role in personal finance, influencing your ability to borrow money for large purchases or emergencies.

A strong credit score can secure loans with favorable terms, saving you money on interest. Building good credit involves paying bills on time, keeping credit utilization low, and maintaining a mix of credit types.

Regularly checking your credit report for errors ensures accuracy. Poor credit can limit financial opportunities and result in higher borrowing costs.

Responsible credit management is essential for maintaining financial health and accessing resources when needed.

Capital

Capital represents the financial resources you invest to generate wealth, including savings, investments, and income-generating assets.

Building capital starts with disciplined saving and smart investment choices. Diversifying investments across stocks, bonds, real estate, and other asset classes minimizes risk and maximizes returns.

Capital growth benefits from compounding, where returns on investments generate further returns over time. Liquid capital, like savings, provides flexibility, while fixed capital, like property, contributes to long-term wealth.

Strong capital reserves offer security, enabling financial independence and the ability to seize opportunities.

Collateral

Collateral refers to assets used to secure loans, reducing risk for lenders. Common types of collateral include real estate, vehicles, or savings accounts.

Pledging collateral allows borrowers to access funds at lower interest rates due to reduced lender risk. However, failure to repay the loan can result in the loss of the collateralized asset.

Assessing the value and importance of assets before using them as collateral is critical. Understanding loan terms and maintaining a strong repayment plan helps protect your assets.

Collateral provides borrowing leverage but requires careful financial planning.

Conditions

Conditions encompass external factors that impact your financial decisions and outcomes, such as economic trends, interest rates, inflation, and market stability.

Favorable economic conditions, like low unemployment and stable markets, create opportunities for saving and investing.

Conversely, high inflation or rising interest rates can increase costs and reduce purchasing power.

Staying informed about economic trends helps you adjust your financial strategies.

For instance, refinancing during low-interest-rate periods can lower debt costs. Adapting to changing conditions ensures resilience and continued progress toward financial goals despite external challenges.

What Are the 5 Main Components of Personal Finance?

The five main components of personal finance are:

Income

Income is the foundation of personal finance and represents the money you earn to support your lifestyle and financial goals.

It includes primary sources such as salaries, business profits, and pensions, as well as secondary sources like rental income, dividends, and side hustles.

A steady income allows you to budget effectively, save for emergencies, and invest for the future.

Tracking your income helps you understand your earning capacity and identify areas for growth. Maximizing income through career advancement or additional revenue streams can accelerate financial success.

Ensuring consistency and reliability in income sources is key to long-term stability.

Expenses

Expenses are the costs you incur to maintain your lifestyle and meet obligations. They are typically divided into fixed expenses, like rent and utilities, and variable expenses, such as groceries and entertainment.

Understanding your spending habits is essential for effective money management.

Categorizing and tracking expenses helps you identify areas where you can cut back and prioritize savings. Creating a realistic budget ensures that your expenses don’t exceed your income.

Monitoring monthly costs also helps avoid unnecessary debt and supports achieving financial goals without compromising your standard of living.

Savings

Savings are the portion of your income set aside for future needs and emergencies.

Building an emergency fund with 3-6 months of living expenses is a crucial first step. Savings also support short-term goals, like vacations, and long-term objectives, such as buying a home or retirement.

Automating contributions to a savings account ensures consistent progress without the temptation to spend. High-yield savings accounts and certificates of deposit (CDs) can help grow your savings faster.

Regularly reviewing and increasing your savings rate is essential as your income grows or financial needs change.

Investments

Investments involve putting your money to work in assets like stocks, bonds, mutual funds, and real estate to grow wealth over time.

They are essential for achieving long-term financial goals, such as retirement or education funds.

Diversification across asset classes reduces risk and enhances returns. Compounding, where your earnings generate additional returns, makes early and consistent investing critical.

Investment strategies should align with your risk tolerance and financial objectives.

Regular portfolio reviews and adjustments ensure that your investments stay on track to meet your goals.

Protection

Protection includes insurance and other safeguards to shield against financial loss.

Health, life, auto, and home insurance are critical to covering unexpected costs and protecting assets.

An emergency fund serves as an additional layer of financial security. Estate planning tools like wills and trusts ensure your wealth is passed on according to your wishes.

Protection strategies also include risk management for investments to mitigate potential losses.

By proactively addressing risks, you can maintain financial stability and prevent unforeseen events from derailing your progress.

Proper protection ensures peace of mind and long-term security.

What Are the 4 Pillars of Personal Finance?

The four pillars of personal finance are:

1. Budgeting

Budgeting is the cornerstone of personal finance, ensuring you allocate your income effectively.

It involves tracking your earnings, expenses, and savings to create a financial plan that supports your goals. Tools like spreadsheets or apps such as Mint and YNAB can simplify the process.

A good budget prioritizes necessities, like housing and food, while leaving room for discretionary spending and savings.

The 50/30/20 rule is a popular guideline: 50% for needs, 30% for wants, and 20% for savings. Regularly reviewing and adjusting your budget ensures it reflects changes in your financial situation.

2. Saving

Saving is essential for building financial security and achieving long-term goals. It starts with creating an emergency fund, typically 3-6 months of living expenses, to cover unexpected costs.

Savings also extend to short- and medium-term goals, like vacations or buying a home. High-yield savings accounts can help grow your funds faster than traditional accounts.

Automating savings through direct deposits ensures consistent progress without relying on discipline.

Over time, savings provide a financial cushion, reducing stress and enhancing stability.

3. Investing

Investing is key to growing wealth and achieving financial independence.

Unlike saving, investing involves putting money into assets like stocks, bonds, or real estate to earn returns over time.

Start by understanding your risk tolerance and financial goals. Diversifying your portfolio across asset classes reduces risk and maximizes returns.

Low-cost index funds and ETFs are ideal for beginners seeking steady growth.

Regularly review your investments to ensure they align with your goals.

4. Debt Management

Managing debt effectively is critical for financial health. High-interest debt, like credit cards, should be prioritized for repayment to minimize interest costs.

Strategies like the snowball or avalanche method can help pay off debt faster. Responsible use of credit, such as paying balances in full and on time, maintains a healthy credit score.

Refinancing or consolidating loans can reduce interest rates and simplify payments.

Good debt, like a mortgage or student loans, should be approached strategically to leverage its benefits while minimizing costs.

The Importance of Personal Financial Planning: Why You Need a Solid Plan

Personal financial planning is essential for achieving financial success. Here are the top reasons why financial planning matters:

Helps You Reach Your Goals

Financial planning provides a roadmap to achieving both short-term and long-term financial goals.

Whether it’s buying a home, starting a business, or saving for your children’s education, a well-defined plan helps you break down these big aspirations into manageable steps.

By setting clear priorities and deadlines, you ensure your money is working toward the most important objectives.

Regular reviews and adjustments to your plan keep you on track as circumstances change.

Achieving your goals becomes a structured process rather than an uncertain ambition.

Improves Money Management

A solid financial plan helps you gain control over your spending and savings.

It encourages tracking every dollar and ensures that your expenses align with your income.

By setting limits on discretionary spending, you can better allocate funds to savings or investments.

Money management becomes intentional, helping you avoid impulse purchases and unnecessary debt.

Regularly reviewing your budget and spending habits improves discipline and decision-making.

This not only increases savings but also enhances overall financial stability.

Prepares You for Retirement

Retirement planning is a critical component of long-term financial security.

By starting early and contributing consistently to retirement accounts, you can build a substantial nest egg.

A financial plan helps determine how much you need to save to maintain your desired lifestyle after retirement.

It accounts for inflation, healthcare costs, and other potential expenses. Different investment options, such as 401(k)s, IRAs, and pensions, can be evaluated to maximize your retirement savings.

Planning ensures that you’re not left scrambling in your later years but enjoy a comfortable retirement.

Reduces Stress

Having a clear financial plan reduces uncertainty and the anxiety associated with money.

Knowing where your money is going and where it should go next helps you feel more in control of your financial future.

Planning for emergencies, such as job loss or medical expenses, provides a safety net. It gives you peace of mind, knowing you’re actively working towards your financial goals and preparing for the unexpected.

This sense of security can reduce the mental and emotional stress caused by financial uncertainty.

Protects Against Risks

A comprehensive financial plan includes protection against life’s uncertainties.

This means having the right insurance coverage—health, life, auto, and home—to shield you from financial disasters.

Emergency funds, ideally covering 3-6 months of living expenses, serve as a financial cushion during unexpected events like job loss or medical emergencies.

By proactively planning for risks, you can minimize the financial impact of unforeseen circumstances.

A well-rounded plan ensures that you’re prepared for the unexpected without derailing your financial progress.

Types of Personal Finance

Personal finance isn’t one-size-fits-all. There are several types and approaches to managing money:

Traditional Personal Finance

Traditional personal finance focuses on the fundamental principles of budgeting, saving, investing, and debt management.

It involves creating a budget to track income and expenses, saving for short-term and long-term goals, and investing to grow wealth.

Managing debt responsibly is also key, ensuring that high-interest debts are paid off while maintaining a balanced financial portfolio.

This approach provides a holistic view of an individual’s finances, aiming to establish stability and secure financial well-being over time. It’s a broad approach that can be tailored to different income levels and financial goals.

Debt Management

Debt management centers on strategies for reducing and eliminating high-interest debt, such as credit cards and payday loans.

Techniques like the debt snowball (paying off the smallest balances first) or debt avalanche (paying off the highest-interest debt first) can help expedite repayment.

It also includes consolidating or refinancing debt to lower interest rates and streamline payments.

A key focus is maintaining a healthy credit score while ensuring that debt does not hinder financial progress.

Building a strategy to avoid taking on excessive debt in the future is also crucial for long-term financial health.

Investment Planning

Investment planning focuses on growing wealth through diversified investment portfolios.

It includes choosing between different asset classes like stocks, bonds, mutual funds, and real estate to create a balanced approach that matches risk tolerance and financial goals.

The strategy may involve setting up retirement accounts like 401(k)s and IRAs or individual brokerage accounts. Risk management and regular portfolio rebalancing are critical elements of this approach.

Investment planning aims to build long-term wealth and financial security by making smart investment choices tailored to an individual’s financial objectives and timeline.

Retirement Planning

Retirement planning is about building savings and investments to ensure a comfortable retirement.

It includes contributing to retirement accounts like 401(k)s, IRAs, and pensions while considering the ideal retirement age and lifestyle.

A key component is estimating retirement expenses, such as healthcare, housing, and daily living costs, to ensure you have enough savings.

This approach also includes tax-efficient strategies for drawing down retirement funds and ensuring that the money lasts throughout retirement.

Retirement planning ensures that you can enjoy financial freedom in later years without relying on others or being financially stressed.

Tax Planning

Tax planning focuses on strategies that minimize taxes and maximize tax savings.

It includes understanding tax brackets, deductions, credits, and tax-advantaged accounts like IRAs, 401(k)s, and HSAs.

Effective tax planning involves timing income, deferring taxes, and taking advantage of capital gains rates or tax-loss harvesting strategies.

The goal is to reduce taxable income while still contributing to savings and investments.

Tax planning also takes into account future tax obligations and the potential impact of life changes like marriage or having children.

It helps individuals keep more of their earnings and ensure financial stability.

Conclusion: Achieving Financial Freedom in 2025

Achieving financial freedom in 2025 begins with taking deliberate steps toward mastering personal finance.

It requires understanding the foundational principles, such as budgeting, saving, investing, and managing debt, while leveraging modern tools to streamline these processes.

By focusing on the 5 C’s of Personal Finance—control, clarity, consistency, commitment, and creativity. You can build a solid financial strategy that aligns with your unique goals. Setting clear, actionable objectives ensures that your efforts remain focused and measurable.

Start today by assessing your financial health, creating a realistic plan, and committing to consistent action. With the right mindset and strategies, financial freedom in 2025 can become a reality, setting the stage for long-term stability and prosperity.

Hasnain Aslam is a seasoned finance blogger and digital marketing strategist with a strong expertise in SEO, content marketing, and business growth strategies. With years of experience helping entrepreneurs and businesses boost their online presence and maximize organic traffic, he specializes in crafting high-impact content that ranks on search engines and drives real results. His insights empower professionals to build sustainable digital success through strategic marketing and innovative SEO techniques.